OYO Rooms Files For IPO: Pre-IPO Review

Oravel Stays Limited, popularly known as OYO Rooms, has filed its Draft Red Herring Prospectus (DHRP) with the Securities and Exchange Board of India (SEBI). The papers filed by OYO are not final and give only insight into its intention, business model, and the challenges it faces before the IPO. The loss-making company with a valuation of close to USD 9 Billion has to confront its own set of challenges before going ahead with a successful IPO. The company plans to raise close to Rs 8,430 crore through its IPO, expected to launch by year-end. This piece analyses the current position of OYO and the challenges it has to tackle before it debuts on the stock market.

Where Does The Company Stand?

- OYO was started in 2012 by CEO Ritesh Agarwal at the ripe young age of 20. The company provides short-stay accommodation, mainly targeting budget travelers. OYO has more than 1.57 lakh storefronts (properties/hotels) across more than 35 countries listed on its platform, with India, Malaysia, Indonesia, and Europe contributing to more than 90% of the total revenue.

- During inception, OYO used to lease hotels at a particular price and rent them out on their platform for a specific rate. This model later, however, changed to a commission-based revenue model. OYO charges around 25-30% commission on most bookings.

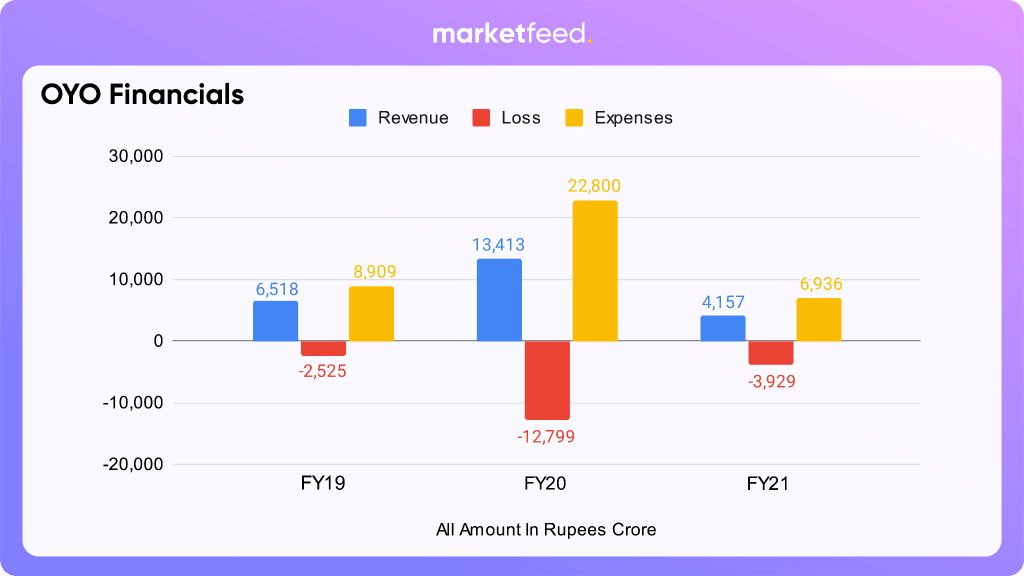

- The company continues to operate at a loss. Post COVID-19, the company’s total revenue, net loss, and expenses all dipped by ~70% between FY 20 and FY21. The Gross Booking Value fell by 66.9% in the same period, and revenue from contracts with customers declined by 69.9%.

- In the post-COVID-19 period, the company has clearly managed to trim its expenses and play it safe. The company made plenty of layoffs, imposed pay cuts, and restructured the company’s management, leading to a ~63% reduction in employee benefit expenses in FY21. Marketing and promotion expenses were cut down by ~71% in the same period.

Complex Structure and Shareholding Pattern

- OYO has 80 subsidiary companies out of which 12 are yet to commence operations. Apart from that, it has 40 Joint Ventures out of which 35 have commenced operations. Many of these companies are shell companies registered in a few of the many Caribbean islands.

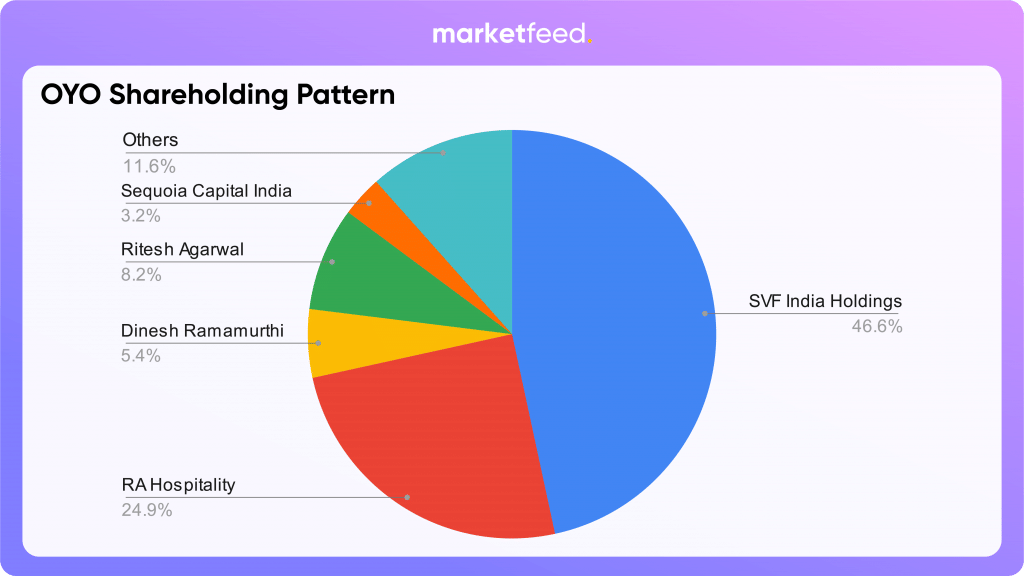

- The company has a complex shareholding pattern. SVF India Holdings is an offshore company of SoftBank that owns close to 46.9% stake in the company. SVF India Holdings is wholly owned by SVF Holdings (UK) LLP. Apart from Ritesh Agarwal’s 8.2% stake in the company, he set up RA Hospitality Holdings (Cayman), an offshore company that owns a 24.9% stake in OYO. OYO uses these offshore companies to raise funding.

- If OYO were to get listed, retail investors would be far less likely to understand the transactions made within the group company. OYO’s complex shareholding and group structure makes it opaque in the eyes of a common investor, is it time for OYO to simplify the company’s structure shareholding?

What Challenges Does The Company Face?

- The COVID-19 pandemic has severely impacted the hospitality industry as well as OYO’s business. Any adverse changes in the situation could continue to affect OYO’s business.

- The company has consistently recorded net losses since incorporation. The company’s ability to achieve profitability might be delayed.

- Inability to retain existing Patrons and Customers or cost-effectively acquire new Patrons and Customers could impact the company’s business and finances. The company has been in dispute with many existing storefront owners who claim that OYO takes an unfair commission and has delayed or denied payment. Some hotel unions have even called for a ban on OYO in certain areas.

- The company is “foreign-owned and controlled” under the Consolidated FDI Policy and FEMA Non-debt Instruments Rules. It is subject to certain foreign investment restrictions, limiting its ability to attract foreign investors and its ability to raise foreign capital is subject to certain conditions prescribed under Indian laws.

- Any adverse outcome in legal proceedings involving Zostel may materially and adversely affect the company’s business, reputation, prospects, results of operation, and financial condition.

Zostel Vs OYO - A Key Concern

In 2015, OYO and Zostel’s subsidiary ZO Rooms were in talks for a merger. The two signed a term sheet in 2015 where Zostel promised to transfer a part of its business to OYO. In return, Zostel and its lead investor Tiger Global were promised a 7% stake in OYO. The deal however did not come into effect ultimately. Zostel claims that it has already transferred the agreed part of the business to OYO, but has not received the promised 7% stake.

After plenty of disputes, disagreements, and problems, the two companies filed a series of criminal and civil complaints against each other. Later, the Delhi and Gurgaon High Court ruled in favor of OYO, after which Zostel appealed to the Supreme Court. The Supreme Court asked the two parties to settle the dispute through arbitration. In 2021, the Arbitral Tribunal ruled in favor of Zostel and asked OYO to transfer the promised 7% stake to Zostel.

With a winning hand, Zostel has now planned to approach SEBI and stall the IPO till OYO does not execute the deal signed in 2015, giving Zostel a 7% stake in the IPO. If OYO ultimately decides to provide Zostel with a stake, the shareholding pattern of OYO will be in a complete mess, ultimately impacting other critical shareholders of the company.

You can read the official arbitration order here.

Where Will OYO Use The Money Raised From The IPO

OYO plans to raise Rs 8,430 crore from its IPO, out of which Rs 7000 crore will be a fresh issue of shares. The remaining Rs 1,430 crores will be an Offer For Sale(OFS) of existing shareholders, which include - SVF India Holdings (Cayman) Limited, A1 Holdings Inc, China Lodging Holdings (HK) Limited, and Global IVY Ventures LLP. Founder Ritesh Agarwal is not going to dilute his stake in the company.

The company plans to use the net proceeds from the sale to:

- Pay off debt worth Rs 2441 crore. As of July 2021, OYO has a consolidated debt of Rs 4,890 crore

- Use Rs 2,990 crore for expansion and organic growth

- Use the remaining amount for General Corporate Purposes.

OYO’s IPO has too many problems starting at its face. Poor finances, legal disputes, and complex company structure, to name a few. The world is staring at inflation, high oil prices, and power shortages. OYO will have to balance its expenses to steer past this rough patch. The only thing that is keeping its IPO buzz alive is the IPO bull run. If the IPO launches when the IPO bull run is still on, investors can expect a fair share of listing gains. If the IPO launches after the US Fed rate hike, global markets shall contract altogether, eventually impacting any IPO, let alone OYO’s. Do you think OYO’s IPO will be a smooth sail? Let us know in the comment section in the marketfeed app available for Android and iOS.