Jargons

How to Know if Financial Statements are Reliable? Audit Reports Explained!

Audit reports provide an independent review of a company's financial statements, offering an opinion on their fairness and reliability. They are crucial for stakeholders making investment decisions and ensuring transparency.

On this page

Key takeaways

- An audit is an independent review of a company’s financial statements conducted by a Certified Public Accountant (CPA) or a qualified Chartered Accountant (CA).

- Audit reports provide reasonable assurance that financial statements are free from material errors and omissions, verifying them for discrepancies.

- A standard audit report contains a title, addressee, Management’s Responsibility, Auditor’s Responsibility, Opinion, Basis of Opinion, Other Reporting Responsibilities, signature, place of signature, and date.

- Types of audit opinions include Unmodified/Unqualified/Clean, Modified, Qualified, Adverse, and Disclaimer of Opinion.

- Internal controls are processes a company uses to ensure accurate financial statements, and auditors express an opinion on their effectiveness.

A company effectively communicates important performance data to its stakeholders through financial statements. These statements form the primary basis for investment decisions. But how do we know if the financial statements provided by the company are reliable? That's where audit reports come in! In this article, we will discuss what audit reports are, their contents and the types of audits. We will also learn what internal controls are.

What is an Audit?

An audit is an independent review of a company’s financial statements. A Certified Public Accountant (CPA) or a qualified Chartered Accountant (CA) conducts audits of companies. An auditor provides an opinion on the fairness and reliability of financial statements. The Board of Directors of companies appoints the auditors, but they should be independent of the firms. The management will not have any control over the auditor.

What is an Audit Report?

We know that the auditor has to provide an opinion. But what exactly does an auditor look for in these statements?

They examine the financial statements and see if they conform to applicable standards, confirm the assets & liabilities of a company, and generally observe if the statements are free from material errors or misrepresentations. Moreover, auditors also examine the company’s accounting and internal control systems. Finally, the auditor expresses his opinion through an Audit Report.

Are Auditing and Audit Reports Important?

In most countries, it is a statutory requirement for publicly listed companies to publish their financial statements every quarter and at the end of a financial year. There are many stakeholders whose decisions depend on these statements. But what if a company’s management alters or modifies these statements to make them look good in front of everyone? What if the company inflates its profits to mislead users? Who verifies them?

Audit reports provide a reasonable assurance that the presented financial statements are free from material errors and omissions. Auditors verify the financial statement for discrepancies.

To stop the management from misleading its stakeholders by modifying these statements, the Companies Act 1956 requires all registered companies to conduct an audit of the financial statements and present it in the form of an audit report at the annual general meeting (AGM).

What are the Contents of an Audit Report?

An audit report contains a title, addressee, Management’s Responsibility for Financial Statements, Auditor’s Responsibility, Opinion, Basis of Opinion, Other Reporting Responsibilities, the signature of the auditor, place of signature, and date of the audit report.

A standard auditor’s opinion contains three parts and states the following:

1. While the financial statements are prepared by management and are its responsibility, the auditor has performed an independent review.

2. Generally accepted auditing standards were followed, thus providing reasonable assurance that the financial statements contain no material errors.

3. The auditor is satisfied that the statements were prepared according to accepted accounting principles and that the chosen principles and estimates made are reasonable.

The auditor’s report contains additional explanations when accounting methods have not been used consistently between periods. It also has a section called Key Audit Matters, which highlights accounting choices that are of the greatest significance to users of financial statements.

Types of Audit Opinions

The different opinions that an auditor may provide are:

- Unmodified or Unqualified or Clean Opinion: This indicates that the auditor believes that the statements are free from material omissions and errors.

- Modified Opinion: Any opinion other than an unmodified/unqualified opinion is referred to as a modified opinion.

- Qualified Opinion: If the statements make any exceptions to the accounting principles, the auditor may issue a qualified opinion and explain these exceptions in the audit report.

- Adverse Opinion: If the statements are not presented fairly or are materially nonconforming with accounting standards.

- Disclaimer of Opinion: If the auditor is unable to express an opinion, they may issue a disclaimer opinion.

The auditor’s opinion will also contain an explanatory paragraph when a material loss is probable, but the amount cannot be reasonably estimated. These types of disclosures may be a signal of serious problems and may call for close examination by an analyst.

How to Analyse Audit Reports?

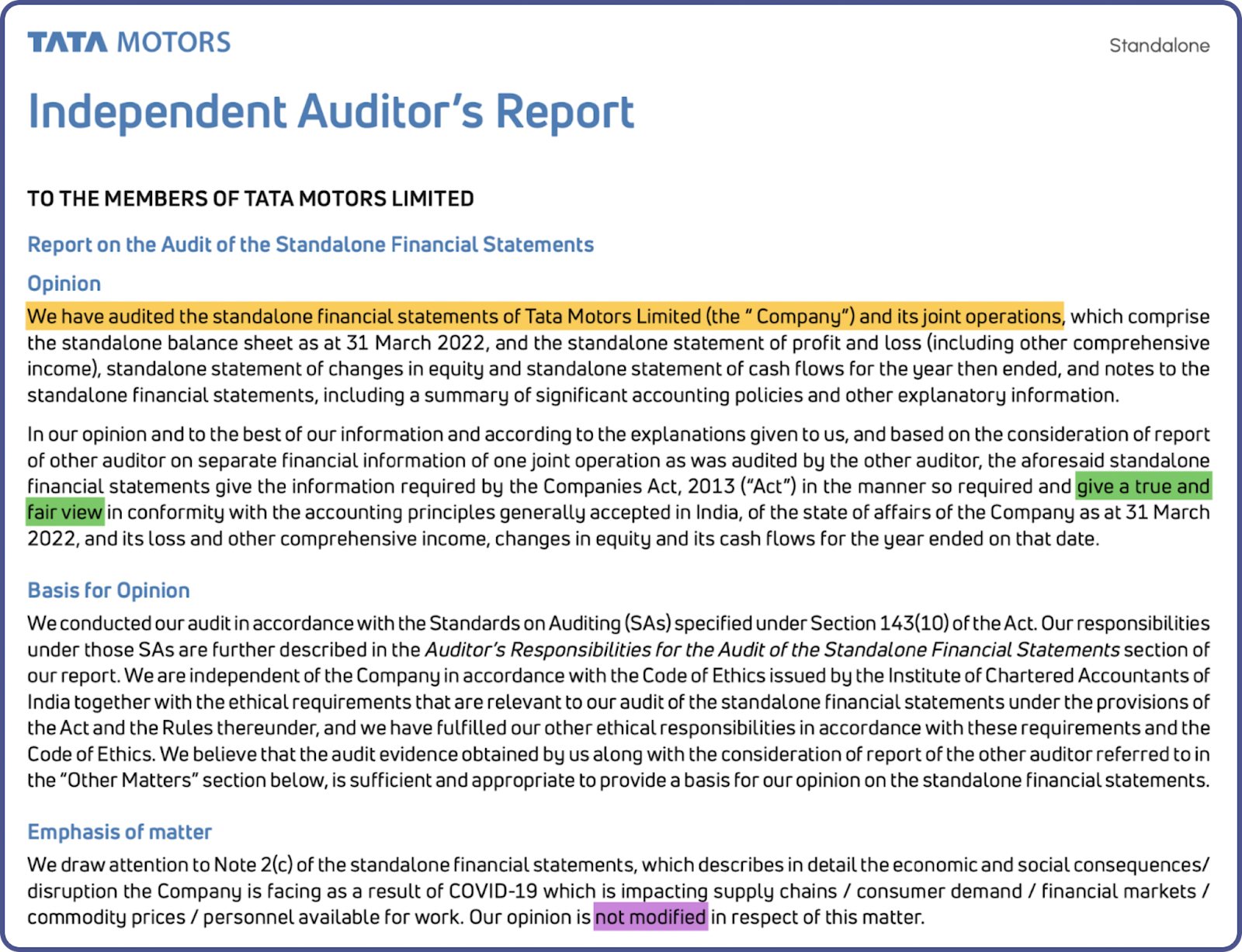

Now that we know the theoretical part, let’s take a look at the Auditor’s Report of Tata Motor’s Standalone Financial Statements for the financial year 2020-21:

Even though the auditor’s report may look different from one company to another, the structure remains the same.

The yellow highlight states that an independent auditor has audited the standalone financial statements.

The green highlight states that the company has complied with the applicable accounting standards and gives a true and fair view.

The violet highlight states the opinion of the auditor is unmodified or unqualified, which is a positive sign. It implies that the auditor believes the statements are free from material errors and omissions.

What are Internal Controls?

Internal controls are the processes by which a company ensures that it presents its financial statements accurately. It is the responsibility of the management to implement and look over its internal controls. However, the auditor must express an opinion about the effectiveness of the implemented internal control measures.

Are Interim Financial Statements Audited?

We had a brief look at the audit report of annual financial statements, but a company also publishes its results or interim financial statements quarterly as well. Are those audited?

Auditing is a rather long process that takes up a lot of time and resources. It is not possible to independently conduct an audit in such a short time. It is also rather expensive. So quarterly financial statements are not required by law to be audited. However, an auditor generally reviews them. Such reviews have limited testing procedures.

In conclusion, audit reports provide an auditor’s opinion on financial statements. Investors should integrate the analysis of audit reports into their financial analysis practices. Make sure to take a look at audit reports when you go through the annual report of any company to verify that the presented financial statements are fair and reliable!

Frequently asked questions

What is an audit?

An audit is an independent review of a company’s financial statements, typically conducted by a Certified Public Accountant (CPA) or a qualified Chartered Accountant (CA).

What does an auditor look for in financial statements?

Auditors examine financial statements to see if they conform to applicable standards, confirm assets and liabilities, observe if statements are free from material errors or misrepresentations, and examine the company’s accounting and internal control systems.

Are interim financial statements audited?

No, interim financial statements are not required by law to be audited because auditing is a long and resource-intensive process, but an auditor generally reviews them.

What are internal controls?

Internal controls are the processes by which a company ensures that it presents its financial statements accurately.

Written by

marketfeed TeamRelated reads

What are Technical Indicators: Definitions and Types?

Understand technical indicators: what they are, how to plot them, their types (overlays, underlays, lagging, leading), and tips for effective use in trading.

What is Volume in the Stock Market? How to Analyse It?

Understand stock market volume, its purpose, and how to use it for trend confirmation. Learn about the Volume Profile Indicator and practical applications for trading.

The BEST Framework to Create a Diversified Stock Portfolio

Learn the best framework to create a diversified stock portfolio for long-term success. Understand asset, market cap, and sectoral diversification for optimal returns.

Join 2.4M+ Indians · Free · 2 min